How to Qualify for Medicaid in West Palm Beach: A 2026 Strategic Guide

- Kelly Mata

- Apr 15

- 13 min read

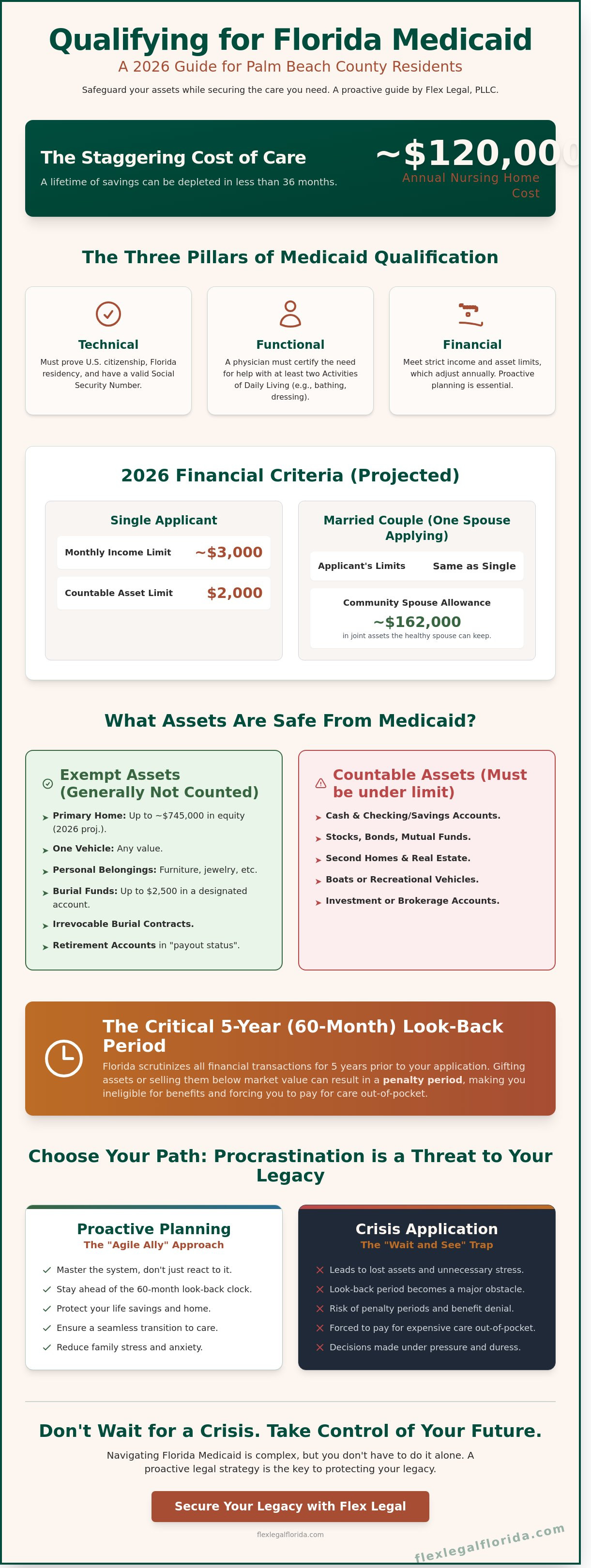

In 2025, the average annual cost for a private nursing home room in Florida has climbed toward $120,000, a figure that can deplete a lifetime of savings in less than 36 months. You likely feel that protecting your family’s inheritance while securing necessary care is an impossible balancing act. The complexity of Florida's 60 month look-back period and the strict asset limits set by the Department of Children and Families often create more anxiety than answers.

We believe legal support should be a transparent partnership rather than a confusing hurdle. This guide provides the clarity you need on how to qualify for Medicaid in West Palm Beach without sacrificing your home or financial independence. You'll discover the 2026 financial thresholds and the modern legal strategies that safeguard your assets while ensuring you meet every eligibility requirement. We'll walk through the application roadmap, from income caps to asset protection trusts, so you can move forward with confidence and a clear plan for your future.

Key Takeaways

Navigate Florida’s specific Long-Term Care Managed Care program with a modern strategy that balances state requirements with your personal needs.

Learn how to qualify for medicaid by mastering the updated 2026 financial thresholds and asset limits tailored for Palm Beach County residents.

Explore proactive asset protection strategies, such as Personal Service Contracts, to secure your legacy without sacrificing necessary benefits.

Streamline the complex Miller Trust process with a clear, step-by-step approach to managing excess income through a dedicated West Palm Beach account.

Identify and bypass common application errors within the ACCESS Florida portal to ensure a seamless transition into the Medicaid system.

Table of Contents Medicaid Eligibility in Florida: More Than Just a Financial Test The 2026 Financial Criteria for Palm Beach County Residents Asset Protection Strategies: Qualifying Without Losing Your Home Step-by-Step: The Qualified Income Trust (Miller Trust) Process Applying for Medicaid in West Palm Beach: Avoiding Common Pitfalls

Medicaid Eligibility in Florida: More Than Just a Financial Test

Florida Medicaid isn't a simple welfare program. It's a complex partnership between state resources and the federal Medicaid program. In the Sunshine State, long-term care is primarily delivered through the Statewide Medicaid Managed Care (SMMC) program. Specifically, the Long-Term Care Managed Care (LTCMC) component provides essential services to seniors in nursing homes or those receiving care in their own homes. Understanding how to qualify for medicaid requires looking far beyond a person's bank account. It's a multi-layered process that demands a strategic, proactive approach.

Most families wait until a health crisis hits to seek help. This traditional "crisis application" often leads to lost assets and unnecessary stress. We advocate for an "Agile Ally" approach. This means we treat Medicaid planning as a dynamic strategy rather than a static set of rules. We help you pivot before the 60-month clock becomes an obstacle. By staying ahead of the regulations, we ensure you don't just react to the system but master it.

The Three Pillars of Medicaid Qualification

Qualification rests on three distinct benchmarks that every applicant must meet. First is the Technical pillar. West Palm Beach applicants must prove U.S. citizenship or qualified alien status, Florida residency, and provide a valid Social Security Number. Second is the Functional pillar. The state uses a "Level of Care" assessment, typically documented via Form 3008. A physician must certify that the applicant requires help with at least two activities of daily living, such as bathing, dressing, or eating. Finally, there's the Financial pillar. While income and asset caps adjust annually, the 2026 landscape will likely see income limits hovering near $3,000 per month and countable assets capped at $2,000 for an individual. Strategic planning is the only way to stay under these limits without losing your life savings.

Why "Wait and See" Is a Dangerous Strategy

Procrastination is the biggest threat to your legacy. Florida enforces a strict 5-year look-back period for any asset transfers. If you've gifted money to grandchildren or sold a home below market value within this timeframe, the state may impose a penalty period. This is a duration where you're ineligible for benefits, forcing you to pay out-of-pocket for expensive care. Knowing how to qualify for medicaid means respecting this timeline. The look-back period is a 60-month window of financial scrutiny. Any uncompensated transfers discovered during this audit can trigger months of disqualification. Planning early ensures your assets remain protected and your transition to care is seamless when the time comes.

The 2026 Financial Criteria for Palm Beach County Residents

Understanding how to qualify for medicaid in 2026 requires a clear look at the numbers. Florida maintains strict thresholds for both income and assets. For a single applicant, the monthly gross income limit for 2026 is projected at approximately $3,000, adjusting for recent inflation trends from the previous $2,829 baseline. If you are a married couple and both are applying, this limit applies to each spouse individually. The asset limit remains at a tight $2,000 for individuals. This means any cash, stocks, or property exceeding this amount could trigger a denial.

For married couples where only one spouse seeks care, the rules offer more breathing room. The "Community Spouse Resource Allowance" (CSRA) allows the non-applicant spouse to keep a significant portion of the couple's joint assets. In 2026, this allowance is approximately $162,000. This protection ensures the spouse remaining at home isn't left in a state of financial depletion. Distinguishing between "countable" assets like second homes or brokerage accounts and "non-countable" assets is the first step in a strategic plan.

What Assets Are "Safe" From Medicaid Scrutiny?

The Florida Homestead remains one of the most powerful tools for asset protection. Your primary residence is generally exempt if your equity is below the 2026 limit of $745,000, provided you or a spouse reside there. You can also keep one vehicle of any value and personal effects like jewelry or furniture. Irrevocable burial contracts and up to $2,500 in designated burial funds are also safe. Retirement accounts are more complex; they are often exempt if they are in "payout status," meaning you are receiving regular, required distributions that count toward your monthly income. Navigating these categories requires a precise inventory of your holdings to ensure nothing is misclassified.

The "Income Gap" Problem in Florida

Florida is strictly an "Income Cap" state. Unlike "Medically Needy" states, you cannot simply spend down your excess income on medical bills to qualify for long-term care. If your monthly income exceeds the $3,000 threshold by even one dollar, you are technically ineligible. This creates a hurdle for many Palm Beach County seniors who earn too much for Medicaid but too little to afford private nursing home rates. Solving this often involves special needs planning or a Qualified Income Trust. You can find a detailed breakdown of these categories on the official site for Florida Medicaid eligibility. If you feel stuck between these limits, our team can help you identify a flexible path forward that preserves your legacy while securing the care you need.

Learning how to qualify for medicaid doesn't have to be a process of total divestment. By identifying which assets are exempt and addressing the income gap early, you can protect your family's future. Modern legal strategies focus on adaptability, ensuring your plan stays robust even as state figures shift each year.

Asset Protection Strategies: Qualifying Without Losing Your Home

Many families mistakenly believe they must exhaust every penny before they can access long-term care benefits. This "spending down" approach often leads to unnecessary financial depletion. In Florida, the 2024 asset limit for a single applicant is just $2,000. However, strategic restructuring offers a more sophisticated path. Instead of losing wealth, you reallocate it into exempt categories that protect your legacy while ensuring you meet the requirements for how to qualify for medicaid.

Strategic restructuring involves several modern legal tools. A Personal Service Contract allows you to pay a family caregiver for future services, effectively transferring assets out of your name while keeping the funds within the family unit. These contracts must reflect fair market value to satisfy state auditors. Additionally, Medicaid-compliant annuities can convert a lump sum of cash into a steady stream of income for a spouse, bypassing the strict asset caps. Flex Legal, PLLC acts as your agile ally in this process, providing the clarity needed to handle these complex financial shifts without the friction of traditional legal models.

When you're ready to start the formal process, Applying for Medicaid in West Palm Beach requires precise documentation of these transfers to avoid penalties during the five-year look-back period. Our team ensures every move is documented and compliant.

The Lady Bird Deed: A Florida Real Estate Secret

The Lady Bird Deed, or Enhanced Life Estate Deed, is a staple for West Palm Beach homeowners. It allows you to retain total control over your property during your lifetime while ensuring the home transfers automatically to your heirs upon death. This avoids the lengthy probate process and, crucially, protects the home from Medicaid estate recovery. Unlike a revocable trust, which doesn't always provide the same level of immediate Medicaid protection for the primary residence, the Lady Bird Deed keeps the home as an "exempt asset." It's a seamless solution for those who want to protect their biggest investment while learning how to qualify for medicaid without selling the family house.

Special Needs Trusts and Disability Planning

For applicants with disabled family members, the "Sole Benefit" rule provides a powerful exception to transfer penalties. You can transfer assets into a Third-Party Special Needs Trust (SNT) for the benefit of a disabled child or spouse without triggering a period of ineligibility. This ensures your loved ones are cared for without jeopardizing their own government benefits. Working with a specialized attorney for special needs trust is vital to ensure the language meets strict federal and state guidelines. These trusts are not just about money; they're about providing a flexible, secure future for those who need it most.

Step-by-Step: The Qualified Income Trust (Miller Trust) Process

Florida uses a strict "income cap" system for long-term care benefits. If your monthly income exceeds the limit, which is $2,829 as of 2024, you're technically ineligible for assistance. This creates a stressful gap for seniors who make too much for Medicaid but not enough to pay for $10,000 monthly nursing home bills. A Qualified Income Trust (QIT) provides a strategic solution to this problem. It's a legal vessel that siphons excess income to maintain Medicaid eligibility.

When Do You Need a Miller Trust?

You need a Miller Trust when your gross monthly income is even one dollar over the state limit. The math is straightforward: take your total monthly income and subtract the current $2,829 cap. The resulting number is your required monthly deposit. This trust must be irrevocable to satisfy the Department of Children and Families (DCF) requirements. Because you can't cancel or change the trust once it's active, the state views that "excess" money as no longer belonging to you. This is a critical step in learning how to qualify for medicaid when your Social Security or pension checks are too high.

Setting Up the Trust Account

The process moves quickly once the legal documents are drafted. You'll need to follow these steps precisely to ensure your application stays on track:

Execute the legal document: A tailored trust document must be signed and notarized to establish the legal framework for the income.

Open a dedicated QIT bank account: Take the trust document to a bank in West Palm Beach to open a zero-balance or low-fee checking account specifically for the trust.

Deposit the excess income: Every single month, you must transfer the "overage" amount from your personal account into the QIT account.

Pay allowed expenses: The funds in the trust aren't lost. They're used to pay for a personal needs allowance, health insurance premiums, or a portion of the nursing home's "patient responsibility" cost.

Common Mistakes in Managing a QIT

Precision is vital for maintaining your status. One common error is failing to fund the trust in the very first month you apply for benefits. If the deposit isn't made, the application will be denied for that month. Another frequent mistake is co-mingling personal funds with trust funds. You shouldn't use the trust account for groceries or gas. Finally, maintain precise monthly record-keeping. DCF performs an annual review, and they'll expect to see a clear paper trail of every deposit and disbursement. Understanding these administrative details is a major part of how to qualify for medicaid without facing unnecessary delays. If you need a modern, streamlined approach to managing these requirements, contact Flex Legal Florida for a consultation.

Applying for Medicaid in West Palm Beach: Avoiding Common Pitfalls

The Florida Department of Children and Families (DCF) manages the gateway to long-term care benefits through the ACCESS Florida portal. While this digital system is designed for efficiency, the application process remains rigorous. You'll need to provide a meticulous "Paper Trail" that accounts for every financial move made over the last 60 months. This includes 5 years of bank statements, property records, and tax returns. Missing a single transaction record can trigger a denial or a lengthy delay. Understanding how to qualify for medicaid involves more than just meeting asset limits; it's about proving your financial history is transparent and compliant with state rules.

The Local Landscape: DCF and Palm Beach County Resources

Palm Beach County residents have access to several local hubs to facilitate their applications. The DCF service center located at 111 S. Sapodilla Avenue in West Palm Beach serves as a primary site for document verification and in-person inquiries. Additionally, the Area Agency on Aging of the Palm Beaches offers localized support for seniors navigating the complexities of long-term care. While these offices provide the necessary forms, they don't offer the strategic planning required to protect your home or savings. Local asset protection lawyers act as the essential bridge between your family and the state. We ensure your trust is structured correctly so that DCF recognizes your eligibility from day one.

What to Expect After You Submit

Once your application is submitted, the wait begins. In Palm Beach County, the typical timeline for an eligibility determination ranges from 45 to 90 days. During this window, DCF caseworkers frequently issue a "Request for Information" via Form 2235. This document usually demands additional proof of a specific asset or a clarification on a past transfer. You must respond to these requests within the strict deadlines provided, or your application will be closed. Even after you're approved, the state requires an annual redetermination. This yearly check-up ensures you still meet the income and asset criteria. We help our clients maintain a streamlined record-keeping system to make these annual updates seamless and stress-free.

Navigating the intersection of state bureaucracy and financial planning requires an agile ally. If you're concerned about how to qualify for medicaid while preserving your family's hard-earned wealth, don't leave the outcome to chance. Our team provides the modern, strategic oversight needed to secure your future. Schedule a consultation with Flex Legal to streamline your application and protect your legacy today.

Take Control of Your Future Care Today

Securing long term care in Palm Beach County doesn't have to mean exhausting your life's savings. As the 2026 financial criteria take effect, it's clear that successful planning requires more than just meeting a basic income test. Utilizing Florida specific tools like Lady Bird Deeds and Qualified Income Trusts allows you to protect your primary residence while staying within state limits. Mastery over how to qualify for medicaid is about using these modern legal strategies to your advantage before a crisis occurs.

Flex Legal Florida brings a fresh, solution oriented perspective to the complexities of elder law. We prioritize your comfort with flat fee options and a streamlined process that removes the friction from traditional legal services. Our team serves as your agile ally, providing the expertise needed to navigate Miller Trusts and asset protection with total transparency. Secure your legacy and your care; contact Flex Legal for a strategic Medicaid consultation.

You've built a life worth protecting, and the right strategy ensures it stays that way. Reach out today to start building a flexible plan that puts your needs first.

Frequently Asked Questions

Can I qualify for Medicaid if I own a home in West Palm Beach?

Yes, you can qualify for Medicaid while owning a home in West Palm Beach if it's your primary residence. For 2024, Florida law exempts your homestead if your equity value is under $713,000. This protection ensures you don't have to sell your house to access long-term care. If your equity exceeds this limit, we explore strategic options like a lady bird deed to maintain your eligibility status.

What is the "look-back" period for Florida Medicaid in 2026?

The look-back period for Florida Medicaid in 2026 is 60 months. This means the Department of Children and Families reviews every financial transfer you made in the five years before your application. Any gifts or asset transfers for less than fair market value can result in a penalty period. Planning early is the most efficient way to understand how to qualify for Medicaid without facing these delays.

How much money can I have in the bank and still qualify for Medicaid?

You can typically have no more than $2,000 in countable assets to qualify as an individual applicant. For married couples where both spouses apply, this limit increases to $3,000. Countable assets include your checking accounts, savings, and stocks. We help clients restructure these funds into exempt assets or specialized trusts to meet the strict financial requirements while preserving your family's hard-earned wealth.

Is a Miller Trust the same as a Special Needs Trust?

A Miller Trust isn't the same as a Special Needs Trust. You use a Miller Trust, or Qualified Income Trust, specifically to manage monthly income that exceeds the state's limit. A Special Needs Trust focuses on protecting assets for a disabled individual so they don't lose access to government benefits. Each tool serves a distinct, strategic role in a tailored plan for your future care.

Can Medicaid take my house after I pass away in Florida?

Florida's Medicaid Estate Recovery Program can file a claim against your estate after you pass, but your home is usually protected. If the property is legally classified as homestead and passes to your heirs, it's generally exempt from these recovery efforts. Using a lady bird deed or a life estate deed provides a seamless way to transfer ownership while avoiding the complex probate process entirely.

What happens if my income is only $10 over the limit?

If your income is even $10 over the 2024 limit of $2,829, you'll need a Qualified Income Trust to remain eligible. This legal document allows you to deposit the excess income into the trust, making it invisible during the eligibility review. It's a standard, reliable solution that ensures a tiny surplus doesn't block your access to the nursing home care or home services you need.

Do I need an attorney to apply for Medicaid in Palm Beach County?

You don't need an attorney to apply for Medicaid in Palm Beach County, but it's a smart choice for complex financial situations. The application process requires 60 months of bank statements and an understanding of evolving state regulations. Partnering with an agile legal team helps you navigate the paperwork with clarity and ensures you're using every available exemption to protect your family's future.

Can I transfer my car to my child to qualify for Medicaid?

You don't need to transfer your car to your child because Florida Medicaid already exempts one primary vehicle of any value. Transferring the title for less than what the car is worth could be flagged as a gift during the 60 month look-back period. Understanding these specific asset rules is a vital part of learning how to qualify for Medicaid while keeping your property in the family.

Comments